Managing multiple loans or a high monthly EMI can put unnecessary pressure on your finances. Whether you have a personal loan, home loan, business loan, or credit card debt, paying large EMIs every month can affect your savings and lifestyle. The good news is that there are several legal and practical ways to lower your monthly EMI without violating any banking rules.

In this guide, you'll learn How to reduce monthly EMI legally, understand different loan management strategies, and discover how making the right financial decisions can help you regain control over your monthly budget.

Why Is Your Monthly EMI So High?

Many borrowers struggle with high EMIs because of:

- Multiple personal loans

- High-interest credit card dues

- Short repayment tenure

- High interest rates

- Multiple lenders with different repayment dates

If your EMI consumes a significant portion of your monthly income, it's time to explore How to reduce monthly EMI legally using safe financial strategies.

1. Increase Your Loan Repayment Tenure

One of the easiest ways to lower your EMI is by extending your loan tenure. When the repayment period increases, your monthly installment decreases.

Benefits

- Lower monthly financial burden

- Better cash flow management

- No legal complications

- Easier budgeting

However, remember that extending the loan tenure may increase the total interest paid over the life of the loan. Always calculate the overall cost before making a decision.

2. Refinance Your Existing Loan

Loan refinancing allows you to replace your current loan with a new one offering a lower interest rate. This is one of the most effective methods for borrowers searching for How to reduce monthly EMI legally.

Refinancing works well if:

- Interest rates have fallen

- Your credit score has improved

- Another lender offers better loan terms

Lower interest rates directly reduce your monthly EMI and may also decrease your overall repayment amount.

3. Transfer Your Loan to Another Bank

A balance transfer allows you to move your existing loan from one lender to another offering lower interest rates and better repayment terms.

Advantages include:

- Reduced EMI

- Lower interest rates

- Better customer support

- Flexible repayment options

Before transferring your loan, check processing charges and compare the total savings.

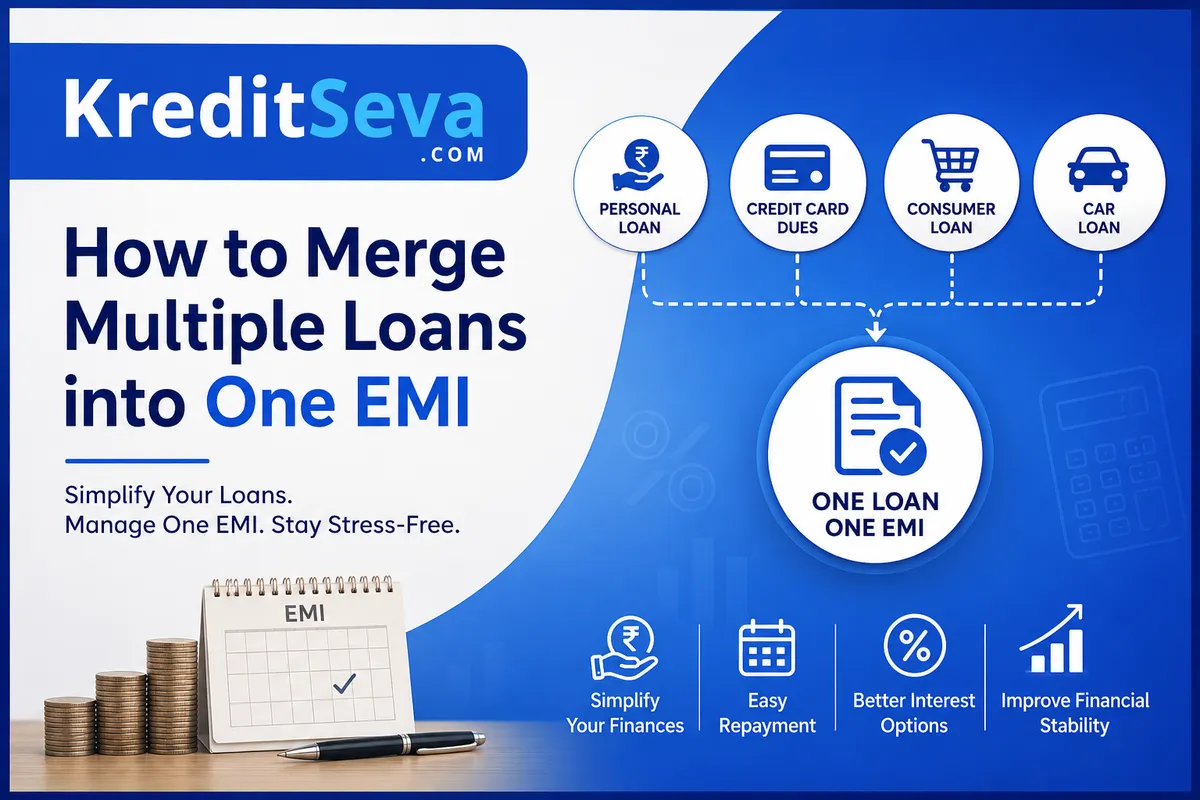

4. Consolidate Multiple Loans into One EMI

If you're paying several EMIs every month, debt consolidation can simplify your finances.

Instead of paying:

- Personal loan EMI

- Credit card EMI

- Consumer loan EMI

- Business loan EMI

You combine them into a single monthly payment.

Many borrowers looking for How to reduce monthly EMI legally prefer debt consolidation because it reduces financial stress while making repayments easier to manage.

Benefits include:

- Single monthly payment

- Lower combined EMI

- Better financial planning

Reduced chances of missing payments

5. Negotiate with Your Lender

Most borrowers don't realize that lenders are often willing to restructure loans for customers with a good repayment history.

You may request:

- Lower interest rate

- Longer tenure

- Temporary EMI reduction

- Loan restructuring

Banks generally prefer restructuring rather than allowing accounts to become overdue.

This is another practical answer to How to reduce monthly EMI legally without damaging your credit profile.

6. Make Partial Prepayments Whenever Possible

Whenever you receive:

- Bonus

- Tax refund

- Incentives

- Business profits

- Extra income

Consider making a partial loan prepayment.

Reducing the outstanding principal lowers future interest, and in many cases, your lender may also reduce your EMI or shorten your loan tenure.

Always check whether your loan has any prepayment charges before making additional payments.

7. Improve Your Credit Score

A higher credit score gives you better bargaining power when applying for refinancing or balance transfers.

You can improve your credit score by:

- Paying EMIs on time

- Clearing credit card balances

- Avoiding loan defaults

- Maintaining a low credit utilization ratio

Borrowers with strong credit profiles often qualify for lower interest rates, making How to reduce monthly EMI legally much easier.

8. Avoid Taking Multiple New Loans

Many people solve one loan problem by taking another expensive loan. This often creates a cycle of debt.

Instead:

- Review your monthly expenses.

- Reduce unnecessary spending.

- Build an emergency fund.

- Focus on paying existing loans first.

Proper financial discipline plays a significant role in reducing EMI-related stress.

Benefits of Reducing Your Monthly EMI

When you successfully learn How to reduce monthly EMI legally, you enjoy several financial advantages:

- Better monthly cash flow

- Lower financial stress

- Improved savings

- Better credit score

- Easier financial planning

- Reduced chances of loan default

- Greater financial stability

Small changes in your loan structure can make a big difference over time.

Benefits of Reducing Your Monthly EMI

When you successfully learn How to reduce monthly EMI legally, you enjoy several financial advantages:

- Better monthly cash flow

- Lower financial stress

- Improved savings

- Better credit score

- Easier financial planning

- Reduced chances of loan default

- Greater financial stability

Small changes in your loan structure can make a big difference over time.

Common Mistakes to Avoid

When trying to lower your EMI, avoid these mistakes:

- Ignoring hidden processing charges

- Extending tenure without calculating total interest

- Missing EMI payments

- Borrowing from unregulated lenders

- Closing old loans without checking penalties

Always compare different repayment options before making any financial decision.

When Should You Consider EMI Reduction?

You should explore EMI reduction options if:

- Your monthly income has decreased.

- You're paying multiple loan EMIs.

- Interest rates have dropped.

- You're struggling to manage household expenses.

- You want better financial flexibility.

Taking action early can help prevent missed payments and long-term financial problems.

Final Thoughts

Learning How to reduce monthly EMI legally is not about avoiding repayment—it's about choosing smarter repayment strategies that fit your financial situation. Options such as refinancing, balance transfers, loan restructuring, debt consolidation, and partial prepayments can significantly reduce your monthly burden while keeping your credit profile healthy.

Before making any decision, compare different lenders, calculate your total repayment cost, and seek professional guidance if needed. A well-planned loan strategy can help you achieve financial stability and peace of mind.

Ready to Lower Your EMI?

If you're looking for expert guidance on reducing your loan burden, KreditSeva is here to help. Our team can assess your financial situation, compare suitable loan options, and recommend the best legal solutions to reduce your monthly EMI. Get in touch today and take the first step toward stress-free loan repayment.