If you've ever cleared a loan EMI or paid off your credit card in full, only to watch your CIBIL score stay frozen for weeks, you're not alone. It's been one of the most common frustrations for borrowers in India — and the Reserve Bank of India has finally stepped in to fix it.

Starting July 1, 2026, the way your credit information gets reported is changing in a big way. Here's everything you need to know, and more importantly, what you should do about it before the deadline hits.

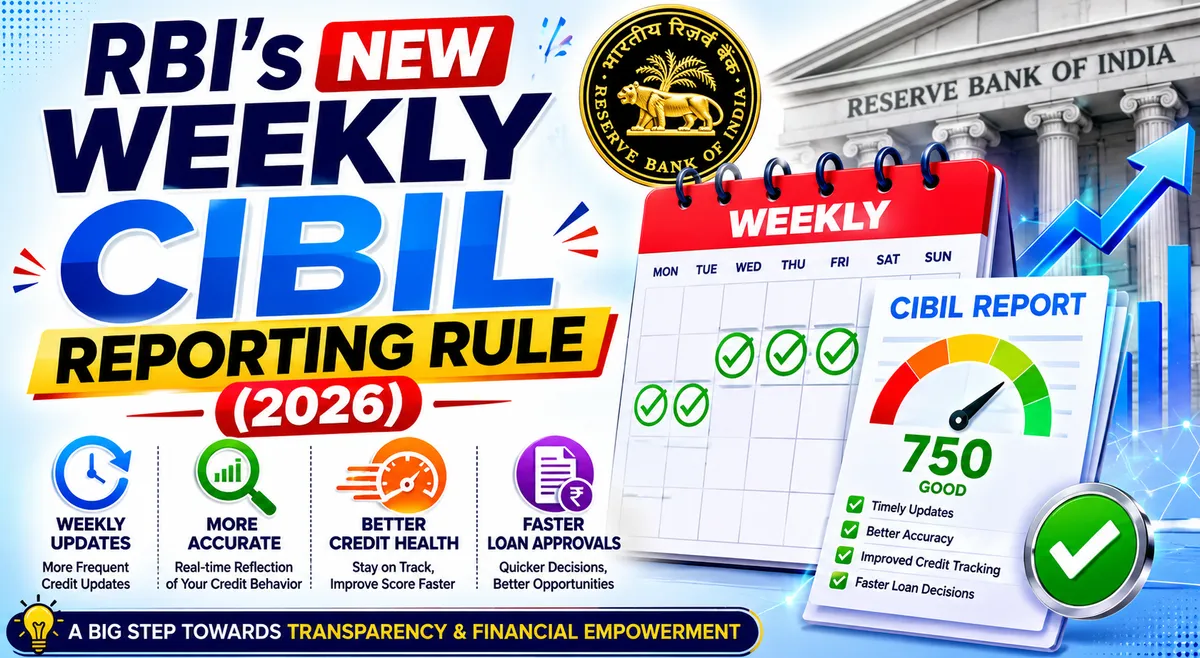

What Exactly Is Changing?

The RBI has amended its Credit Information Reporting Directions to require banks, NBFCs, and other lenders to report borrower data to credit bureaus like CIBIL far more frequently than before.

Under the earlier system, lenders typically reported credit data once a month, sometimes with delays of 30 to 45 days before changes actually showed up in your credit report. Under the new framework, lenders must submit credit information on four fixed reference dates every month — the 9th, 16th, 23rd, and the last day of the month. For changes happening between these dates (a repayment, a closed account, a missed EMI), lenders have to send an "incremental" update within four calendar days of each reference date.

In effect, your credit report can now refresh up to four times a month instead of once — a genuine shift from monthly to near-weekly visibility.

Worth noting: this rule was originally supposed to start on April 1, 2026, but the RBI pushed the deadline to July 1, 2026 after lenders flagged operational concerns, and simplified a few reporting requirements in the process.

Why This Matters to You as a Borrower

This isn't just a back-end compliance change for banks — it directly affects how fast your financial behavior shows up where it counts.

The good news first: if you're a disciplined borrower, your hard work will finally get reflected sooner. Pay off a personal loan today, and instead of waiting a month or more, the update could appear in your credit report within days. That matters if you're planning to apply for a bigger loan, like a home loan, soon after closing smaller debts.

The catch: the same speed applies to mistakes. Miss an EMI or let a credit card bill slip, and that will also reflect in your score much faster than before. The buffer that let occasional slip-ups go unnoticed for weeks is shrinking. Lenders evaluating your loan application will increasingly be looking at your most recent 30–60 days of behavior, not just your history from a year or two ago.

For young borrowers and first-time credit users especially, this is a double-edged sword: it rewards consistency quickly, but it's also less forgiving of carelessness.

What This Means for Different Types of Borrowers

- Salaried professionals and small business owners: Faster reflection of repayments means quicker improvement in eligibility for top-up loans, balance transfers, or better interest rates.

- Credit card users: Utilization ratios and payment timing will be visible to lenders in near real-time, so the old trick of "manage it before the statement date" matters even more now.

- New-to-credit borrowers: Building a clean track record will start showing results faster, which can help you qualify for better terms earlier than under the old monthly cycle.

- Anyone planning a major loan application: If you're closing existing debts to improve your eligibility, the impact will likely show up well before your next loan application, rather than after.

What You Should Do Before July 1, 2026

A few simple steps now will help you make the most of the new system:

- Check your current CIBIL score and report. Know your starting point so you can track changes accurately once weekly updates begin.

- Clear any overdue EMIs or credit card dues immediately. Don't wait — under the new cycle, clearing dues now means a faster visible improvement.

- Set up auto-debit for all your loans and credit cards. With reporting moving faster, even a single accidental missed payment will hurt sooner.

- Keep credit utilization below 30% of your limit. This has always mattered, but it will now be visible to lenders with less lag than before.

- Avoid applying for multiple loans or cards in a short window. Each hard inquiry dips your score, and that effect will also be more immediately visible.

- Review your credit report periodically for errors. Since data is refreshing more often, it's worth checking that lenders are reporting your information correctly.

The Bigger Picture

This change is part of a broader RBI push to make India's credit ecosystem more transparent, accurate, and responsive — alongside other 2026 reforms aimed at faster dispute resolution and stricter timelines for correcting errors in credit reports. Together, these changes are designed to reward disciplined borrowers more quickly while holding both lenders and credit bureaus to tighter accountability standards.

For the millions of Indians who rely on personal loans, credit cards, and EMI-based purchases as part of everyday financial life, this is one of the most consequential — if quietly rolled out — changes to hit the credit system in years.

Final Thoughts

The shift to near-weekly credit reporting is good news if you manage your credit responsibly, and a wake-up call if you've been relying on reporting delays as a safety net. Either way, the smartest move right now is the same one that's always worked: pay on time, keep your utilization low, and check your credit report regularly.

If you're planning to apply for a personal loan and want to know where you stand, check your eligibility with Kreditseva before you apply — it only takes a few minutes, and it helps you avoid unnecessary hard inquiries that could affect your score under the new reporting rules.

Disclaimer: This article is for general informational purposes only and reflects publicly available regulatory information as of June 2026. It is not financial or legal advice. Please refer to official RBI notifications or consult a financial advisor for guidance specific to your situation.