Managing several loans at the same time can quickly become overwhelming. Different repayment dates, varying interest rates, and multiple EMIs can make it difficult to stay on top of your financial commitments. Missing even a single payment may affect your credit score and increase financial stress.

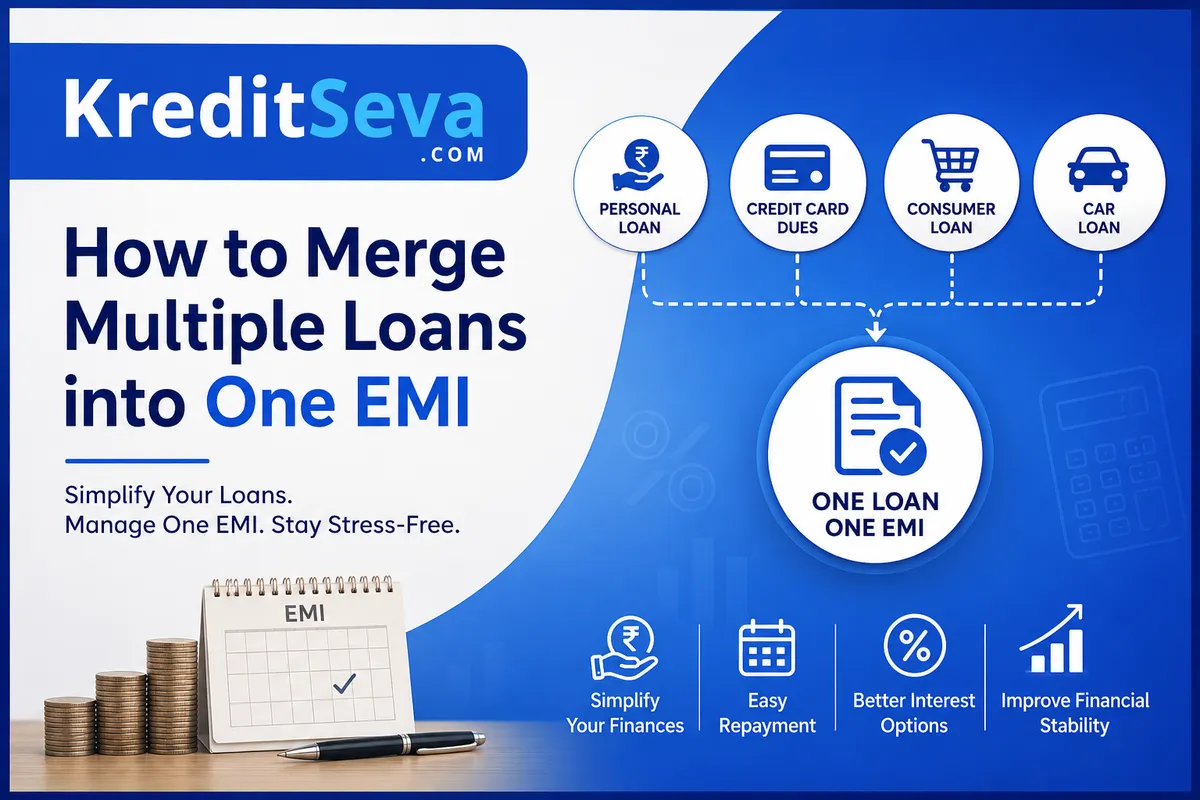

If you're wondering How to merge multiple loans into one EMI, you're not alone. Many borrowers choose loan consolidation to simplify their repayments and improve financial management. By combining multiple debts into a single loan, you only have one monthly EMI to remember, making budgeting much easier.

In this guide, we'll explain how loan consolidation works, its benefits, eligibility, potential drawbacks, and tips to help you make an informed decision.

What Does It Mean to Merge Multiple Loans into One EMI?

When people search for How to merge multiple loans into one EMI, they are usually referring to the process of loan consolidation. Loan consolidation allows you to combine several existing loans—such as personal loans, credit card dues, consumer loans, or other unsecured debts—into one new loan.

Instead of making separate monthly payments to different lenders, you make one EMI to a single lender. This approach can simplify repayment while helping you better organize your finances.

Depending on the lender, the new loan may also offer a lower interest rate, a longer repayment tenure, or more flexible repayment terms.

Why Do People Choose Loan Consolidation?

There are several reasons borrowers decide to consolidate their loans.

One of the biggest advantages is convenience. Managing multiple EMIs every month increases the chances of missing due dates. With only one EMI, repayment becomes much easier.

Another reason is improved cash flow. If the new loan comes with a longer repayment tenure or a lower interest rate, your monthly EMI may become more affordable.

Many borrowers also use debt consolidation to regain control over their finances after taking multiple personal loans, using several credit cards, or financing various purchases separately.

Benefits of Combining Multiple Loans

Loan consolidation offers several practical benefits for borrowers who are struggling with multiple repayments.

Easier Financial Management

Tracking one EMI is much simpler than managing several repayment schedules. It reduces confusion and helps you stay organized.

Better Budget Planning

A single monthly payment makes it easier to prepare your monthly budget and monitor expenses without worrying about different due dates.

Possibility of Lower Interest Costs

Depending on your credit profile and lender, you may qualify for a lower interest rate than your existing loans, reducing your overall borrowing cost.

Reduced Risk of Missed Payments

Missing EMIs can negatively impact your credit score. Consolidation minimizes this risk by reducing the number of payments you need to manage.

Improved Financial Discipline

With only one repayment commitment, borrowers often find it easier to build healthier financial habits and stay consistent with repayments.

Who Should Consider Loan Consolidation?

Loan consolidation isn't suitable for everyone, but it can be a good option if you:

-

Have multiple personal loans.

-

Carry high-interest credit card balances.

-

Struggle to keep track of different EMI dates.

-

Want to simplify monthly repayments.

-

Are looking for better repayment terms.

-

Have a stable income to manage a consolidated loan.

Before making a decision, it's important to compare the overall cost of the new loan with your existing loans.

Steps to Merge Multiple Loans into One EMI

If you're exploring How to merge multiple loans into one EMI, following a structured approach can help you choose the right solution.

1. List All Your Existing Loans

Prepare a complete list of your loans, including:

-

Outstanding balance

-

Interest rate

-

Remaining tenure

-

Monthly EMI

-

Prepayment charges (if any)

This gives you a clear picture of your total debt.

2. Check Your Credit Score

A good credit score increases your chances of getting a better interest rate on the consolidated loan.

Lenders generally offer more competitive terms to borrowers with strong repayment histories.

3. Compare Loan Consolidation Options

Different lenders provide different loan products.

Compare factors such as:

-

Interest rates

-

Processing fees

-

Repayment tenure

-

Pre-closure charges

-

EMI flexibility

Choose an option that genuinely reduces your financial burden rather than simply extending repayment.

4. Apply for the New Loan

Once you've selected the right lender, submit the required documents, such as identity proof, income proof, bank statements, and loan details.

The lender will evaluate your eligibility before approving the consolidation loan.

5. Close Existing Loans

After receiving the new loan amount, ensure all previous loans are fully repaid and obtain loan closure certificates from each lender.

This helps avoid future disputes and keeps your credit report accurate.

Important Factors to Consider Before Consolidating

Although loan consolidation offers many advantages, borrowers should carefully evaluate a few important factors before proceeding.

Total Cost of Borrowing

A lower EMI may seem attractive, but a longer repayment tenure could increase the total interest paid over the life of the loan.

Always calculate the complete repayment amount before making a decision.

Processing Fees

Some lenders charge processing fees or administrative charges that increase the overall borrowing cost.

Prepayment Penalties

Certain loans include foreclosure or prepayment charges. Check these costs before closing your existing loans.

Credit Eligibility

Your loan approval and interest rate depend on factors like your credit score, income, existing debt, and repayment history.

Common Mistakes to Avoid

Many borrowers make avoidable mistakes during loan consolidation.

Some common ones include:

-

Choosing the first lender without comparing offers.

-

Ignoring hidden charges.

-

Extending the loan tenure unnecessarily.

-

Continuing to accumulate new debt after consolidation.

-

Missing payments on the new loan.

A disciplined repayment strategy is essential for making loan consolidation successful.

Can Loan Consolidation Improve Your Credit Score?

Many borrowers ask whether How to merge multiple loans into one EMI can positively affect their credit profile.

The answer depends on how responsibly you manage the new loan.

If you consistently pay your consolidated EMI on time, reduce outstanding debt, and avoid taking unnecessary new loans, your credit score may gradually improve over time.

However, missing repayments on the consolidated loan can negatively affect your credit history.

Alternatives to Loan Consolidation

Loan consolidation is not the only debt management solution.

Depending on your financial situation, you may also consider:

-

Balance transfer options

-

Loan refinancing

-

Debt restructuring

-

Negotiating repayment terms with existing lenders

-

Accelerated repayment using surplus income

Consulting a financial advisor may help you determine the most suitable option for your circumstances.

Tips for Managing a Single EMI Successfully

After consolidating your loans, maintaining healthy repayment habits becomes even more important.

Here are a few practical tips:

-

Set up automatic EMI payments.

-

Maintain an emergency fund.

-

Avoid taking unnecessary new loans.

-

Review your monthly budget regularly.

-

Pay extra whenever possible to reduce the principal amount.

-

Monitor your credit report periodically.

These habits can help you stay financially stable and reduce long-term debt.

Final Thoughts

Understanding How to merge multiple loans into one EMI can help borrowers simplify debt management and reduce financial stress. Loan consolidation offers the convenience of a single monthly payment, improved budgeting, and the possibility of better repayment terms. However, it is essential to compare lenders, understand all associated costs, and evaluate whether consolidation truly benefits your financial goals.

Before making any decision, carefully review your existing loans, calculate the total borrowing cost, and choose a repayment plan that aligns with your income and long-term financial objectives. With responsible borrowing and timely repayments, consolidating multiple loans into one EMI can become an effective step toward achieving greater financial stability and peace of mind.